Options trading can feel overwhelming with all its complex terms and calculations, but learning the basics makes it much easier to understand. One of the most important concepts for both new and experienced traders is option Delta. Delta measures how sensitive an option is to changes in the price of the underlying asset. It shows how much your option’s value is likely to change for every dollar the stock or commodity moves.

You can think of Delta like a speedometer for your option’s price. A speedometer shows how fast your car is moving, and Delta shows how quickly your option’s value changes compared to the underlying asset. A higher Delta means the option reacts more to price changes, while a lower Delta means it reacts less.

What is Delta, Mathematically?

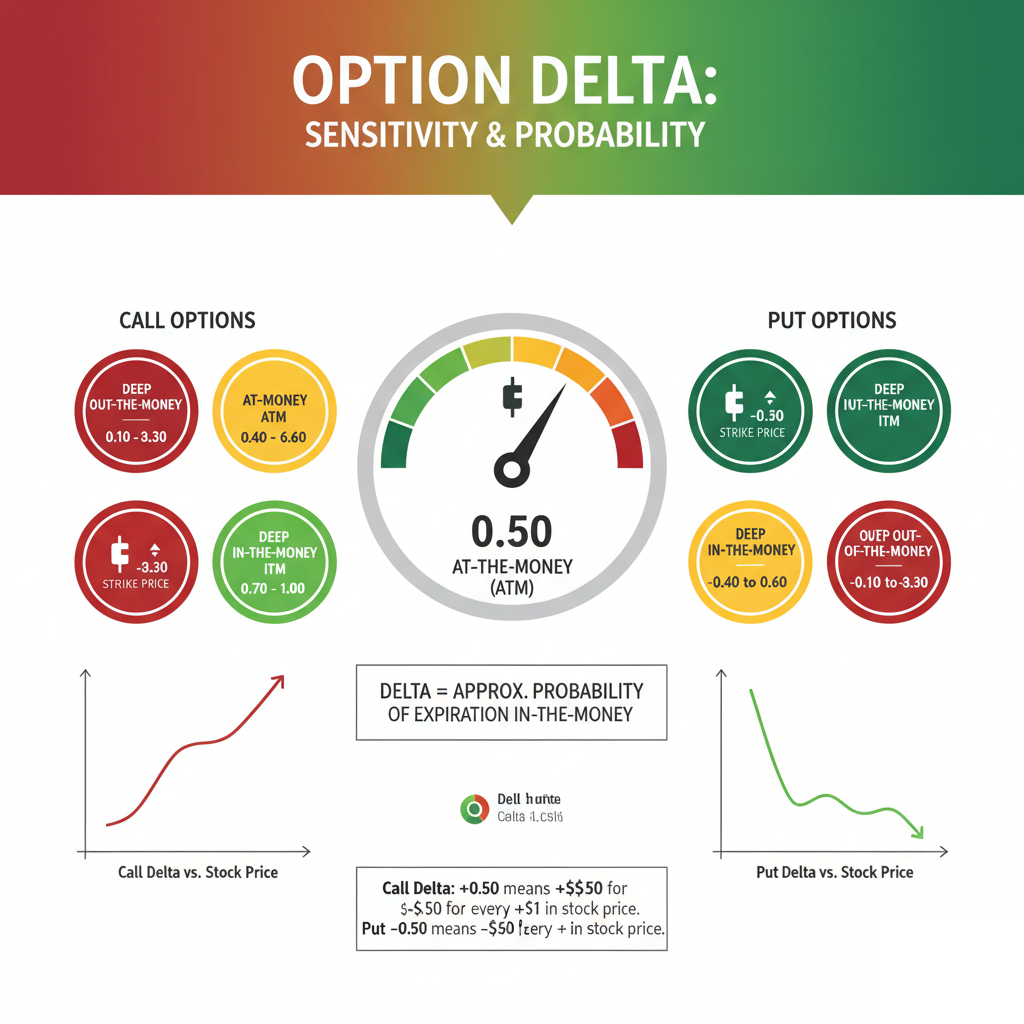

Technically speaking, Delta is one of the “option Greeks,” a set of risk measures used in options trading, and is expressed as a number between 0 and 1 for calls, and 0 and -1 for puts.

- Call Options: A call option with a Delta of 0.50 means that for every $1 increase in the underlying stock’s price, the call option’s value is expected to increase by $0.50. Conversely, if the stock price drops by $1, the call option’s value is expected to decrease by $0.50.

- Put Options: A put option with a Delta of -0.50 implies that for every $1 increase in the underlying stock’s price, the put option’s value is expected to decrease by $0.50. If the stock price falls by $1, the put option’s value is expected to increase by $0.50. The negative sign for put options simply reflects their inverse relationship with the underlying asset’s price.

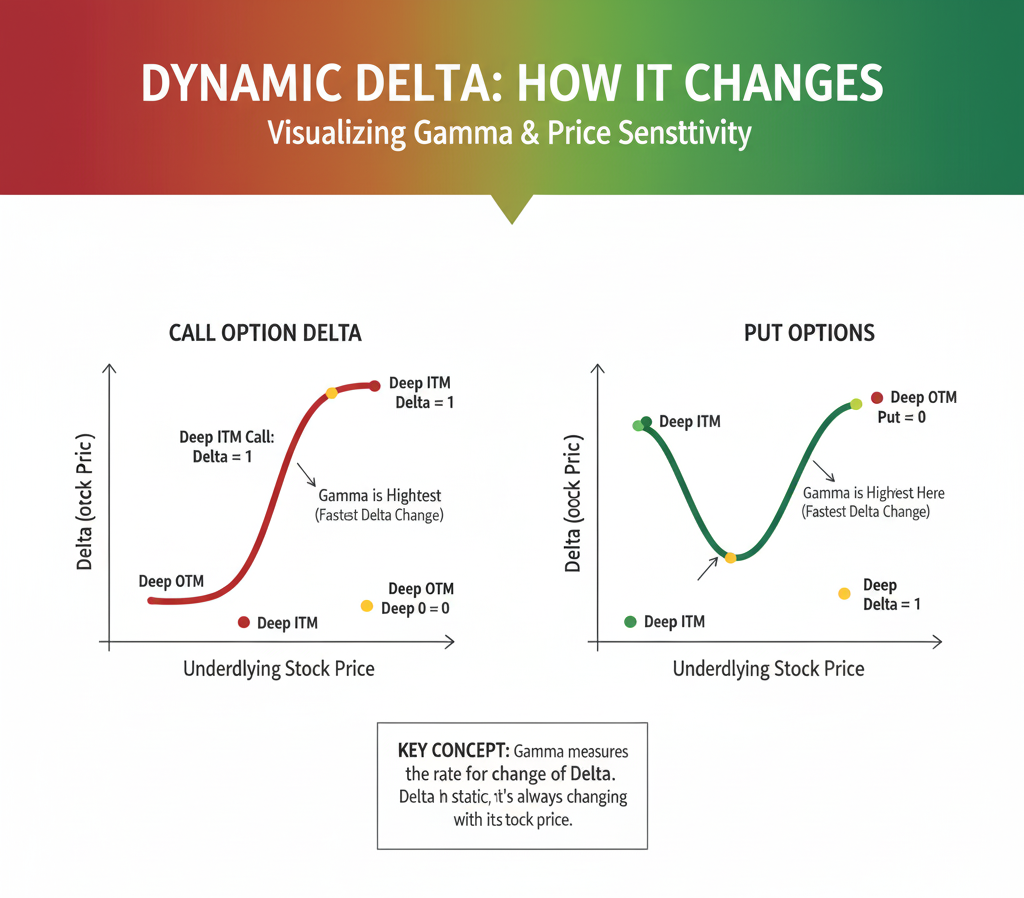

Delta’s Dynamic Nature: It’s Not Static!

It’s crucial to understand that Delta is not a fixed number; it’s constantly changing. Several factors influence Delta, including:

- Moneyness of the Option: This refers to whether an option is in-the-money (ITM), at-the-money (ATM), or out-of-the-money (OTM).

- Deep In-the-Money (ITM) Options: These options have a Delta closer to 1 (for calls) or -1 (for puts). This is because they behave very much like the underlying stock itself. A deep ITM call option’s price will move almost dollar-for-dollar with the stock.

- At-the-Money (ATM) Options: ATM options typically have a Delta close to 0.50 (for calls) or -0.50 (for puts). This is where the uncertainty of the option’s future “moneyness” is highest.

- Deep Out-of-the-Money (OTM) Options: These options have a Delta closer to 0. They are less sensitive to price changes in the underlying asset because there’s a lower probability of them becoming profitable.

- Time to Expiration: As an option approaches expiration, its Delta can change dramatically, especially for ATM and OTM options. Options with more time until expiration generally have a lower Delta than those with less time, assuming all other factors are equal. This is because there’s more time for the underlying price to move, making the outcome more uncertain.

- Volatility: Higher implied volatility generally leads to higher Deltas for OTM options (both calls and puts). This is because increased volatility makes it more likely that an OTM option will eventually move into the money.

Delta as a Probability Proxy

Beyond being a measure of price sensitivity, Delta can also be interpreted as a rough probability that an option will expire in-the-money. While not a precise scientific probability, it serves as a useful heuristic. An option with a Delta of 0.70 for example, might be seen as having approximately a 70% chance of being in-the-money at expiration. This approximation is particularly useful for ATM and OTM options.

Practical Applications for Traders

Understanding Delta has several practical benefits for options traders:

- Risk Management: By knowing an option’s Delta, you can estimate how much your portfolio value might change with movements in the underlying asset. This helps in position sizing and overall risk assessment.

- Hedging: Traders can use Delta to create Delta-neutral portfolios, where the overall Delta of their positions is close to zero. This strategy aims to profit from factors other than directional price movement, such as time decay (Theta) or volatility changes (Vega).

- Directional Trading: For traders with a strong directional view on a stock, choosing options with appropriate Deltas can maximize potential gains. For instance, if you expect a significant upward move, a higher Delta call option will provide more leverage.

- Premium Calculation: Delta is a key component in options pricing models and helps in understanding how much of an option’s premium is intrinsic value versus time value.

Example Scenario:

Imagine you believe Stock XYZ, currently trading at $100, is poised for a modest increase. You’re considering two call options:

- Option A (OTM): Strike price $105, Delta 0.30

- Option B (ATM): Strike price $100, Delta 0.50

If Stock XYZ rises by $2, here’s the estimated impact:

- Option A: Expected to increase by $0.30 * $2 = $0.60

- Option B: Expected to increase by $0.50 * $2 = $1.00

This simple example illustrates how a higher Delta option (Option B) provides more exposure to the directional movement of the underlying stock.

The Delta Range Visualized

Understanding Delta’s Movement

It’s also important to visualize how Delta itself changes as the underlying stock price moves. This concept is captured by another Greek, Gamma, which measures the rate of change of Delta. For now, let’s focus on the general trend:

In conclusion, Delta is a powerful tool in an options trader’s arsenal. By understanding its meaning, how it changes, and its practical applications, you can make more informed trading decisions, better manage your risk, and ultimately enhance your profitability in the dynamic world of options trading. While it might seem complex at first, mastering Delta is a significant step towards becoming a more sophisticated and successful options trader.

Want to master options trading? Delta is just the start! To gain a comprehensive understanding of how all the options Greeks (Delta, Gamma, Theta, and Vega) work together and how to use them to build advanced strategies, click here to access our complete, free options course now and elevate your trading skills.